I am currently running about 2% initial equity risk on each position I enter.

However, and here comes my question: the actual risk I am running in each position shouldn't it rather be the AVERAGE loss of each losing trade than the initial equity risk taken?

I am a discretionary trader and I set stops according to the market, meaning I often immediately adjust stops when my position goes in my way, reducing the AVERAGE loss on losing positions to about 1% of equity. Any opinions ?

I don't understand the question. You seem to be mixing your R-multiple distribution up with initial risk. R is ALWAYS your initial risk on a position. Just because you get to tighten your stops on some trades, doesn't mean anything. Why? Because you never want R to be more than your risk tolerance, in this case 2%.

If your tighter stop gets tapped, and you only lose 1% on that trade, that trade registers a -.5R, instead of a full -1R. That is fine, so long as you stuck to your rules about trailing stops.

I think you are over-thinking this part a bit. Just use 2% (if that meets your objective in connection with your risk tolerance), and keep moving stops according to plan.

Some more questions:

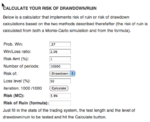

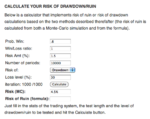

@ fastcar: could you please help me with the explanations of your link? I put in my current stats and received the following:

Prob. Win: 0.40

Win/Loss ratio: 1.72

Risk Amt (%): 2

Number of periods: 10000

Risk of:

Loss level (%): 70

iteration: 1000 /1000

Risk (MC): 0.8% {is this the variance of the MC Sim?}

Risk of Ruin (formula): 3.15% {Is this my probability of a 70% drawdown?}

It means with a 40% win rate and a win/loss ratio of 1.72, risking 2% of your equity on each trade, after 1000 Monte Carlo simulations that include 10,000 trades each your RISK OF RUIN (70%) threshold is .8% and 3.15% respectively, as calculated using the simulator. PLEASE UNDERSTAND RISK OF RUIN IS USELESS, BECAUSE IT IS CALCULATED BASED ON YOUR INITIAL CAPITAL AND ALWAYS TENDS TOWARD ZERO AS YOU ADD MORE TRADES.

For example, you start with 10,000, and are willing to lose 70% of it down to $3000. The first string of trades ARE THE ONLY ONES THAT COUNT because as your equity grows, your chances of drawing down that deep are slim to none. So, lets say you make it to $15,000 - now you would need a an 80% percent draw down to ruin. If you make it to $30,000 you would need a 90% drawdown to ruin. I HOPE YOU CAN SEE HOW LITTLE USE THIS CALCULATION IS WITH RESPECT TO YOUR ONGOING POSITION SIZING STRATEGY. You need to focus on DRAWDOWN as reported by the MC simulations, and determine what your risk tolerance is. I have only come to understand this very well in the last week. I hope this is helpful to you.

@ the hare: regarding re-sampling, do you think it is suitable if you keep your risk fixed to the total equity? Wouldn't that be erratic if you equity grows and you sample larger trade sizes randomly at the beginning ?

I look forward to Hare's input here, but thought I would chime in in case he was tied up: Hare was stating that he uses actual trade results in his MC simulations. This is preferable to the Marble Game, which used fixed R-multiples. In real life, you get many, many results, not just -1R, +1R, +2R etc. This was not emphasized at all by Van Tharp in 'The Definitive Guide to Position Sizing', which cannot be definitive since it leaves more questions than it answers.

Here is also my current 2011 P&L

Image - TinyPic - Free Image Hosting, Photo Sharing & Video Hosting

This is on about 1800 trades so far, net of spreads/commissions; as said I am trading completely discrationary mainly in gold, oil, European Indices and some single stocks on an intraday or 1-3 day basis.

More input and reads regarding position sizing are more than welcome!

Thanks and have a good weekend,

Yuppie

Your trading is going very well. Are you live trading yet? If so, are you keeping track of your efficiency? Van Tharp writes about this in Super Trader, and I think next to position sizing, it's the most important aspect of trading. He states you must be trading at 90% efficiency (1 mistake in 10 - no more than that) to succeed in the long run. Your results appear to evidence good efficiency.

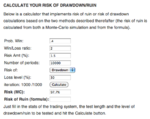

With respect to position sizing I would be very careful with a system that has only 40% winners. Based on 1000 simulations, and 500 trades per year, in a given year your chances of hitting a 50% drawdown are around 62% at 2% risk!!! Would you really be able to stomach that kind of loss? Would it effect your efficiency levels? Many people who experience that much pain begin revenge trading, or taking profits early, or skipping good trades due to fear, etc. and destroy an otherwise good system. You need to give this very careful consideration.

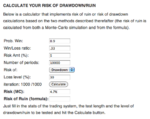

If you back down to 1% risk, your chances of a 50% drawdown are 0% on 500 trades and only 5% for a 33% drawdown (which is still sizable). If it were my account, I'd be using no more than 1%.

If you want more size, without experiencing devastating drawdowns, develop a system with a higher winning percentage. A system with a higher win rate even with a lower win/loss ratio will have a MUCH smoother equity curve, and allow you to safely use more leverage. Go on the simulator and play with a few systems, and see for yourself how much leverage they allow you to use for a given drawdown. This was the Gem I took from Larry C. Sanders white paper. This is something Sanders elucidated, but is lost on Van Tharp. Tharp believes it's ALL ABOUT EXPECTANCY and that you MUST keep losses small, and let winners run. But computer simulations clearly show that a system with a HIGHER WIN RATE, even IF it has a lower win/loss ratio, even if it has a LOWER EXPECTANCY will outperform. Why? Because you can safely use more leverage, and still meet your risk objectives.

Sanders work is the most sensible and comprehensive explanation to position sizing I have come across. In fact, I have so much confidence in his work, that I am no longer studying the subject. (The only thing that would incite me to do further research would be if I were trading a portfolio, rather than taking one trade at a time - which is what his work is based on) Not only does he explain everything you need to know (he even debunks 'optimal-f') but he provides software to do it. His white paper and software put to shame Van Tharp's 'Definitive Guide to Position Sizing' - which leaves the reader completely frustrated, since it leaves the reader with questions as well as offers no clear way to computer model what he discusses.

fastcar