HFM.

Senior member

- Messages

- 2,184

- Likes

- 0

Date 1st September 2023.

Market Update – September 1 – The Calm Before the Storm?

The markets were quiet on the last day of August, awaiting the key jobs report today. Treasuries and the US Dollar were firmer, but off their best levels, while Wall Street closed mixed. Ongoing expectations that the FOMC can pause, or is done with rate hikes continued to support along with the lingering impact from the dovish JOLTS result, the cooling in ADP, and the downward revision to Q2 GDP. Income numbers were in line with expectations, including the pick up in y/y inflation metrics, and hence did not hurt the optimistic Fed outlook. The drop in jobless claims was also overlooked. Month-end buying also supported.

Asian stock markets traded mixed, with Hang Seng and ASX struggling, while JPN225 and CSI 300 nudged higher. Futures are posting fractional gains in Europe and the US, although the US100 is struggling. The 10-year Treasury yield is up 0.4 bp as the all important US jobs report comes into view.

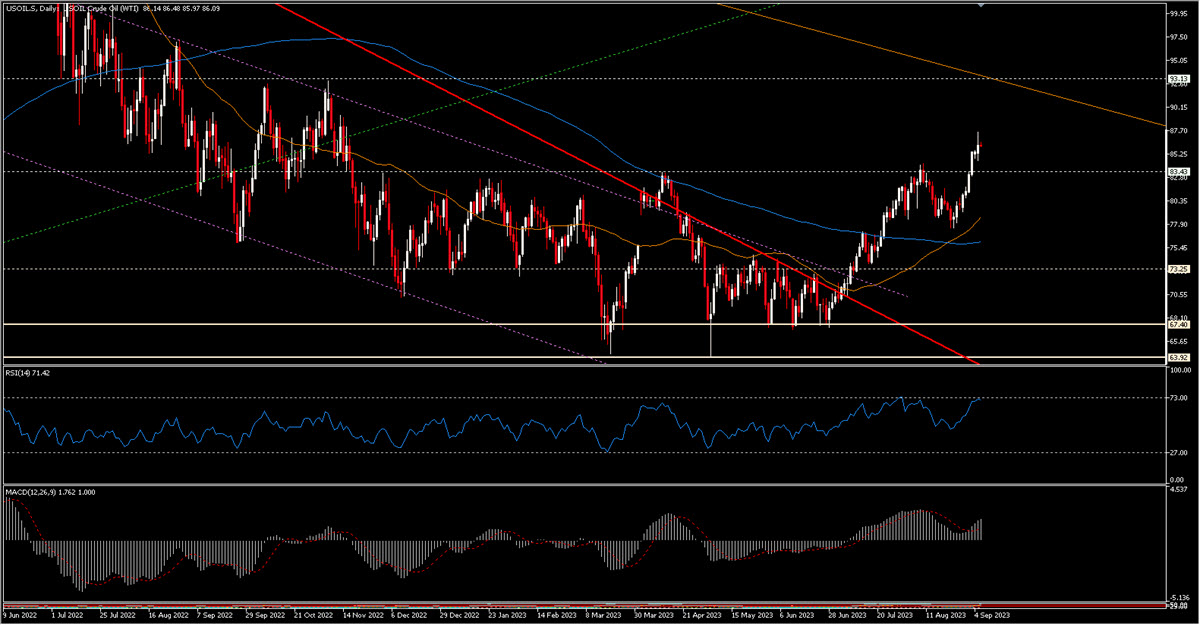

Key Movers: USOil & UKOIL have extended gains by 1.9% to $83.65 and 1.25% to $87.15 respectively as Bloomberg reported Russia has agreed with OPEC+ to extend output cuts.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Click HERE to READ more Market news.

Andria Pichidi

Market Analyst

HFMarkets

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – September 1 – The Calm Before the Storm?

The markets were quiet on the last day of August, awaiting the key jobs report today. Treasuries and the US Dollar were firmer, but off their best levels, while Wall Street closed mixed. Ongoing expectations that the FOMC can pause, or is done with rate hikes continued to support along with the lingering impact from the dovish JOLTS result, the cooling in ADP, and the downward revision to Q2 GDP. Income numbers were in line with expectations, including the pick up in y/y inflation metrics, and hence did not hurt the optimistic Fed outlook. The drop in jobless claims was also overlooked. Month-end buying also supported.

Asian stock markets traded mixed, with Hang Seng and ASX struggling, while JPN225 and CSI 300 nudged higher. Futures are posting fractional gains in Europe and the US, although the US100 is struggling. The 10-year Treasury yield is up 0.4 bp as the all important US jobs report comes into view.

- FX – USDIndex recovered Wednesday’s losses and is currently settled at 103.71, EURUSD turned down to 1.0830, GBPUSD pulled back to 1.2650. Both EUR and Sterling corrected today as markets reined in tightening expectations for BoE and ECB, with yields dropping across the board and Eurozone spreads coming in. US data added further support for the USD as markets assess the interest rate outlook.

- Stocks – Wall Street gave up its gains and faded into the close, leaving the US30 and US500 down -0.48% and -0.16%, respectively, breaking a string of four straight days of gains. The US100 was up 0.11%, higher for a fifth consecutive session.

- Commodities – USOil prices have extended gains with WTI now up 1.9% to $83.65 and Brent 1.25% firmer at $87.15. This is a sixth consecutive session of gains on WTI, the best run since the start of the year. Along with the signs of a still robust US economy, indication of more stimulus from China, and declining stockpiles, Bloomberg reports that Russia has agreed with OPEC+ to extend output cuts. Also, the impacts from Hurricane Idalia are still being assessed.

Key Movers: USOil & UKOIL have extended gains by 1.9% to $83.65 and 1.25% to $87.15 respectively as Bloomberg reported Russia has agreed with OPEC+ to extend output cuts.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Click HERE to READ more Market news.

Andria Pichidi

Market Analyst

HFMarkets

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.