I've read the whole journal and I feel entitled to write one short post with my advice (advice from an unprofitable trader so far).

1) Deadline (of a few weeks) for everything to be ready to be traded with real money? Not a good idea in my opinion. Especially if no one is pointing a gun at you to start trading by then.

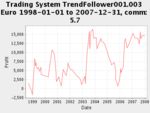

2) I sense you are expecting too much from your systems (a drawdown of a few months on a system is ok, and if you don't want a whole red year, then start testing with intraday data) and this leads to overoptimization, and this in turn leads to systems that don't work and get discarded. I'd rather find a good idea that works and with simple parameters produces no red years, set it aside and move on to the next idea, until you've built a few dozens different systems. By the way, if the same system works on different securities, then it's probably good. Personally I feel it's better to focus on quantity than quality, because that search for quality lead me to overoptimizing, producing worthless systems with a lot of parameters, and wasting a few years.

3) The fewer parameters you use, the more you can trust the system. In the same way, the fewer parameters you use, the more you can allow yourself to optimize them.

4) I am not sure if you mentioned something close to walk-forward optimization. In my experience it's best to optimize in the past 10 to 20 years or so, see if it works, and then use the system as it is. That is only in case you considered using an approach that every once in a while re-optimizes parameters. Personally I don't think it's a good approach.

5) After back-testing and optimizing and finishing a few dozens of simple systems (across as many securities as possible), I would advise to forward-test them (without real money), and keep those that work, or at least record the results for a few months, and at least not trade those that are not working.

6) Don't save money on buying data, in case you are. I found a few people (including myself) who were saving a few hundreds by not buying the needed (intraday) data for backtesting, and were being held back in their tests by that lack of data. Saving a few hundred dollars in this area will make you waste thousands in real trading, so it's not a good idea. So, I would buy all the data you will ever possibly need from the start. A reliable and cheap data provider is disktrading.com. That's what I used.