A reflective sesssion ahead

It promises to be a funny session today, with divergence seen between our opening calls for a weaker ASX 200 (following the weakness in December SPI futures) and BHP and CBA’s American Depository Receipt (ADR), which are higher.

A reflective session was had on Wall Street, with the S&P 500 unchanged, while NASDAQ put on 0.5%. Breadth was poor, with 60% of the S&P 500 lower. Volumes through the S&P 500 were 17% above the 30-day average.

Energy was the underperformer, with the sector -1.2%. US crude reacted to a 567,000 barrel increase in gasoline stockpiles, as opposed to a 559,000 drawdown in actual crude inventories and a 0.8% drop in the refinery utilisation rate. News of Nigeria and Libya bringing more supply on-line was a clear headwind as well. All eyes are watching for a break of the 1 September low of $43.00 for a move into $40.

Volatility has subsided somewhat with the US 10-year treasury falling three basis points to 1.69%, with the VIX +1.6%. Some focus has been on the volatility ETF (VXX), which traded 72 million shares in US trade overnight, and is clearly a weapon of choice for US traders wanting to express a view on volatility. VXX traded 109.7 million shares on Tuesday - more than any S&P 500 company! This is one for the radar.

There has been some interesting developments in US politics, with the wind now to Trump’s back. Trump is now ahead in two different polls in Ohio (Ohio has predicted 16 of the last 17 US elections), Florida (a key swing state) and Nevada. Bring on the first presidential debate on 27 September, where there will surely be fireworks.

Trump is still behind in the betting odds, but it seems Kellyanne Conway’s appointment as campaign manager in mid-August is helping at a time where Hillary’s PR is struggling.

In FX land, the bigger upside moves came from the Scandinavian currencies, with limited moves in EUR or AUD. EUR/USD seems very comfortable in a $1.1200 to $1.1300 range and is obviously focused on next week’s Federal Open Market Committee (FOMC) meet. We also get US retail sales tonight, so keep an eye on the control group element that feeds into the GDP calculation. The market expects +0.4% here.

Technically, the daily chart of the DAX (Germany 30) is at very interesting levels, having pulled back to test the April 2015 trend support.

AUD/USD traded in a tight 45 pip range ($0.7451 to $0.7496) and is clearly eyeing today's August employment report. Consensus is calling for 15,000 net jobs, with the unemployment rate remaining at 5.7%. The analysts range is +45,000 to -18,000, and while the data point is well thought of as a lottery by traders, keep in mind that the AUD is still sensitive to this print. For what it’s worth, the swaps markets are pricing a 30% chance of a cut from the Reserve Bank of Australia (RBA) this year.

The ASX 200 is being called down 15 points, with SPI futures -0.3%. Keep in mind options and futures expiry and roll today, so the December contract becomes front month for the SPI futures and we are likely to see strong volumes through the market, as well the potential for strange price action. Interestingly, if one looks at the ADR’s of BHP and CBA, they are up 1.3% and 1.6% respectively, which doesn’t make much sense for a market likely to open lower.

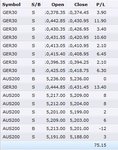

Goldman Sachs have upgraded CBA to a ‘buy’ recommendation (from neutral), setting a price target of $82.79. This suggests ‘stabilizing returns outlook not reflected in valuations’.

It was certainly interesting price action in the ASX 200 yesterday with good buying seen in stocks with a compelling yield, and telcos and financials putting in a strong showing. That could spill over again today, with Goldman’s upgrade of CBA a likely talking point from some investors. Who wouldn’t want a potential 23% total return!

The focus will also be on the Aussie jobs report though, but this is an AUD play at best. I don’t expect this to impact the rates or equity market in any great way. AUD/USD is still holding below the 31 August low and is trending lower, although there has been some indecision on the daily chart to really push price lower from here. Obviously a weaker jobs report changes that.

We have been given little to key off from Wall Street, so it could be somewhat of a reflective session, although it’s worth pointing out the VIX remained firm despite an unchanged read in the S&P 500 cash market. This shows traders still expect elevated volatility over the coming 30 days.