L1 L2 regularizations, dual, bias and bad daughter

Happy New Year !!!

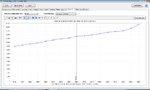

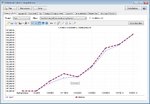

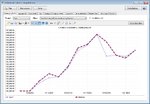

As markets are closed now and my bad daughter refused to play tennis with me i made some investigations about impact of different types of regularization for results of my system. For this I choose algo unfriendly days i.e. 15,16 and 17.12 and EURUSD 1 min when EURUSD broke long term suport level and market behaved very strange. Then I rerun for those days in MATLAB LIBLINEAR classifier with different regularization and bias values

options:

-s type : set type of solver (default 1)

0 -- L2-regularized logistic regression (primal)

1 -- L2-regularized L2-loss support vector classification (dual)

2 -- L2-regularized L2-loss support vector classification (primal)

3 -- L2-regularized L1-loss support vector classification (dual)

4 -- multi-class support vector classification by Crammer and Singer

5 -- L1-regularized L2-loss support vector classification

6 -- L1-regularized logistic regression

7 -- L2-regularized logistic regression (dual)

-c cost : set the parameter C (default 1)

-e epsilon : set tolerance of termination criterion

-s 0 and 2

|f'(w)|_2 <= eps*min(pos,neg)/l*|f'(w0)|_2,

where f is the primal function and pos/neg are # of

positive/negative data (default 0.01)

-s 1, 3, 4 and 7

Dual maximal violation <= eps; similar to libsvm (default 0.1)

-s 5 and 6

|f'(w)|_inf <= eps*min(pos,neg)/l*|f'(w0)|_inf,

where f is the primal function (default 0.01)

-B bias : if bias >= 0, instance x becomes [x; bias]; if < 0, no bias term added (default -1)

-wi weight: weights adjust the parameter C of different classes (see README for details)

-v n: n-fold cross validation mode

-q : quiet mode (no outputs)

and here are the results. BS means BuySell signal i.e. ensembled from2 separate BUY and SELL signals. For each of this signals LIBLINEAR had the same settings