oildaytrader

Senior member

- Messages

- 2,806

- Likes

- 125

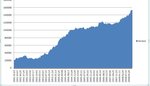

lol says on the repotrt, 7 years!! for 90% roi

12% return per year...yeh great system

and why u backtestig it up to 2008? lol..lets see it up to 2010 thanks, bet its ****

i think this proves you are full or **** and a fraud.

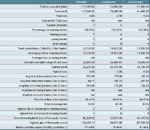

Add 4 different systems with different equity curves, and we have a great combination of systems producing 50% per annum.

I don't back test after 2008, due to lack of data and most brokers switching to 5 digits,but use forward tests and live accounts for testing and trading.

http://www.alpari.co.uk/en/dc/databank.html

Your posts prove only one thing , who is full of it and whose the fraud trying to lure noobs ?.