- US CPI and UK Spring Statement dominate modest data schedule, with Japan

PPI to be digested ahead of US NFIB Small Business Optimism; EcoFin

meeting, Poloz speech and govt bond sales in Italy, Netherlands & USA

- UK Spring Statement: all eyes on OBR report, expected to upgrade budget

and economic outlook

- US CPI: forecasts assume rather dull headline outturn, but a) plenty of

wildcards and b) adverse base effects kick in from March

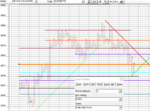

- Charts: US 3-mth Bill Rate vs US 90 Day CP rate; US Money Market Funds

Total Net Assets

..........................................................................

********************

** EVENTS PREVIEW **

********************

The US CPI data and the UK finance minister's inaugural Spring Statement (budget) are the stand-out items on the day's agenda, and are accompanied by the overnight Japan PPI and Australian Housing Finance data and the US NFIB Small Business Optimism survey, as well as govt bond auctions in Italy, Netherlands and the USA. The regular EU EcoFin meeting and a speech by Boc governor Poloz may provide some further points of interest. The other item that will get a lot of attention is the Special Congressional election in Pennsylvania, following the resignation of Rep Tim Murphy (R.) back in October, with the poll of polls suggesting Lamb (Democrat) and Saccone (Republican) are neck and neck. With the mid-term elections due in November, a decisive victory (and the margin will be key) will be interpreted as being as a signal for November, though with around 8 months to go, this may prove to be a case of jumping the gun. Chart of the day - US 3mth Bill Yield (1.67) vs. 90 Day US Commercial Paper rate (2.04), which makes the S&P500 Dividend Yield at 1.84 look rather unappetising.

** U.K. - Spring Statement **

- Having moved the annual Budget statement to November, and affirming that there will be no new fiscal measures announced today, the primary point of interest may well be the OBR's fiscal and economic outlook update. The latter is expected to point to a much better than expected outturn for this year's (2017/18) headline Total Budget deficit (ca. £40 Bln vs. prior £50 Bln), with the Current Balance expected to post a marginal surplus, thanks to stronger revenues (in part due to higher inflation). The OBR sharply downgraded the the UK's potential growth rate back in November, primarily due to weak productivity growth. In the meantime, official data have seen Output Per Hour posting its best two quarter gain since 2008, giving scope for a modest upgrade to the UK's potential growth rate. It should however be stressed that even this improvement still leaves it lagging far behind the pace seen in the 1997-2007 period. On the other side of the fiscal equation, medium and long-term interest rates have risen rather more rapidly than assumed in the November OBR report, which will offset some of the ostensible fiscal head room. Eminently much still depends on what happens with Brexit negotiations, above all the pressing need for a 'transition agreement' to be rubber stamped at the EU council meeting on 22-24 March, rather than being deferred until June. This is above all in so far as any 1 year term business contracts signed after 30 March will bridge the official 29 March 2019 Brexit date, and would thus have to signed in the hope of an agreement, if no transition deal is agreed at the March council meeting. Per se, however many column inches are devoted to today's Statement, the current trend improvement may ultimately be moot, if assumptions about the future outlook are put to the sword by whatever is actually agreed, which could swing in either direction.

** U.S.A. - February CPI **

- Friday's soft Average Hourly Earnings has certainly helped to assuage some inflation concerns, and that impression may be reinforced if today's CPI data match or undershoot expectations of a 0.2% m/m rise on headline and core, which would see headline edge up to 2.2% y/y from 2.1%, and core unchanged at 1.8% y/y. However, a scratch below the surface still highlights that a 0.2% on m/m headline would still equate to a 6-mth annualized rate of 3.6% (with March through June seeing challenging base effects, as readings -0.2%, +0.2%, -0.1% and flat fall out of the comparison. Likewise core CPI would see a 2.2% 6-mth annualized rate, with readings 0.1 -0.1% and three consecutive +0.1% drop out of the comparison in coming months. To be sure, core CPI would on that basis still be well behaved, but still leave real yields looking quite thin in the face of a solid pace of growth and a sharp rise in govt borrowing, even if the FOMC does need to ensure that it is adhering to a symmetric inflation target, i.e. allows for a degree of fluctuation above and below the 2.0% target. In the detail a fall in gasoline prices will likely be offset by a pick-up in food prices, however Household Energy could be a big wild card (given sharp swings in Heating Oil over the month), while housing (OER last 0.3% m/m), Medical Care (0.4% m/m) should continue to pressure core CPI higher. A partial reversal of a steep 1.7% m/m rise in Apparel prices along with the more modest rise in Auto prices in January are likely to be the other key swing factors / wild cards.

from Marc Ostwald