The adaptivity fallacy

You are looking at the transition from one market regime to another one. I would not call it a lag. I would call it persistence.

Persistence = “Continuance of an effect after the cause is removed”

Whereas the term lag applies more to stationary regimes.

>> lag does not depend of m-mistory ???

This is not what I said!!!! I said the lag depends on the reconstruction; it depends on the group you choose. Ultimately if you use 250 components in your group for a full reconstruction, the lag becomes zero. You increased m-histories but you intentionally let the group unchanged making the reconstruction coarser.

Let me now state the obvious right up front:

Most indicators on Earth, (adaptive, non adaptive, oscillators, trendlines) have some persistence as long as there are not computed from thin air!!

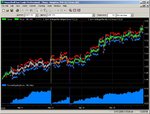

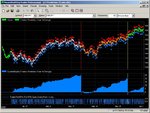

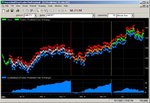

As you can see in the left chart below, the MESA Sinewave indicator fails in exploiting the cycles where CSSA succeeds.

The right chart shows the following:

- The “zero-lag” Instantaneous trendline trails the CSSA cycle by 3 to 4 bars,

- Crossings from MESA Sinwave lag the CSSA cycle by the same amount,

- An adaptive indicator such as Chande’s Vidya can have large persistence,

- The Sinwave persistence appears to be the worst in this small panel.

These results prove you wrong again!!!! You wrote in your post #246:

http://www.trade2win.com/boards/757594-post246.html

>> I found another strong weakness - lack of addaptiveness which I believe was

>> recognized by traders.

>> “So as a summary of those 2 posts we can say that CSSA has a big lag in case of

>> signal change plus will not adapt to not included in training range patterns.”

Instead these results indicate that CSSA-Cycle has no lag, and even if it does not adapt to features not learned, it behaves better than an adaptive indicator to a change in market conditions. It also behaves better that MESA Sinwave!

By stating that CSSA lacks adaptiveness (your post #250, http://www.trade2win.com/boards/757946-post250.html), you imply that adaptiveness is good. Your argument is a fallacy and here is why: adaptive indicators forget as fast as they can to adapt to new features therefore each feature becomes a new feature to them hence they carry a persistence moving forward. CSSA works because, by setting a training range, the user can select the whole data or any part of it to learn from the features he is interested in trading; the cycles can then be set so as to adapt to these features better than any other indicator with no learning capacity.

Noxa

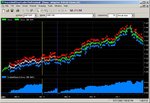

lag does not depend of m-mistory ??? Strange, see screenshot below. The same signal,

two CSSA cycles one with m-history 50 another with 250. It's clear that 250 has bigger lag i.e. time when cycles will disapear from indicator output after disappearing from the signal.

For the readers. After change the signal, the proper output is a flat line of course but this output is delayed due to lag.

Krzysztof

You are looking at the transition from one market regime to another one. I would not call it a lag. I would call it persistence.

Persistence = “Continuance of an effect after the cause is removed”

Whereas the term lag applies more to stationary regimes.

>> lag does not depend of m-mistory ???

This is not what I said!!!! I said the lag depends on the reconstruction; it depends on the group you choose. Ultimately if you use 250 components in your group for a full reconstruction, the lag becomes zero. You increased m-histories but you intentionally let the group unchanged making the reconstruction coarser.

Let me now state the obvious right up front:

Most indicators on Earth, (adaptive, non adaptive, oscillators, trendlines) have some persistence as long as there are not computed from thin air!!

As you can see in the left chart below, the MESA Sinewave indicator fails in exploiting the cycles where CSSA succeeds.

The right chart shows the following:

- The “zero-lag” Instantaneous trendline trails the CSSA cycle by 3 to 4 bars,

- Crossings from MESA Sinwave lag the CSSA cycle by the same amount,

- An adaptive indicator such as Chande’s Vidya can have large persistence,

- The Sinwave persistence appears to be the worst in this small panel.

These results prove you wrong again!!!! You wrote in your post #246:

http://www.trade2win.com/boards/757594-post246.html

>> I found another strong weakness - lack of addaptiveness which I believe was

>> recognized by traders.

>> “So as a summary of those 2 posts we can say that CSSA has a big lag in case of

>> signal change plus will not adapt to not included in training range patterns.”

Instead these results indicate that CSSA-Cycle has no lag, and even if it does not adapt to features not learned, it behaves better than an adaptive indicator to a change in market conditions. It also behaves better that MESA Sinwave!

By stating that CSSA lacks adaptiveness (your post #250, http://www.trade2win.com/boards/757946-post250.html), you imply that adaptiveness is good. Your argument is a fallacy and here is why: adaptive indicators forget as fast as they can to adapt to new features therefore each feature becomes a new feature to them hence they carry a persistence moving forward. CSSA works because, by setting a training range, the user can select the whole data or any part of it to learn from the features he is interested in trading; the cycles can then be set so as to adapt to these features better than any other indicator with no learning capacity.

Noxa