nine

Senior member

- Messages

- 2,049

- Likes

- 510

The Basis of my trading

Futures trading courses and systems are offered for sale at prices ranging from a few hundred dollars to several thousand dollars.

Many of these trading methods are not new or original. Often they are based on information found in trading books or articles written decades ago. In some cases they are old trading methods repackaged in new books (or made into software), and sold at high prices.

The original sources of these methods are sometimes obscure and unknown to the general public.

If you know where to look, however, some of these high-priced futures trading systems can be traced back to their original source - at a much lower price.

And there are some trading methods, of recent design, known only to a few Chicago traders, the few that actually make a living from trading - rather than from hawking books, software, and seminars.

I am an ex-floor trader and broker living in Chicago.

The basis of this system was told to me several years ago by a veteran floor trader at the Mid- America exchange in Chicago. He had two futures accounts: one for his day trading, and another for "position" trading, using this method almost exclusively. He was a millionaire and traded large positions, but he started his career with a small account. He made the millions from the market, using his methods, over several years. (He was a contemporary of Richard Dennis). He didn't mention who created the system.

The system was originally created for position trading. I developed some variations which work for day trading stock index futures.

Variations of this trading system are known to a handful of people in the Chicago trading community. I have been told of one individual who charges $1000 for instruction, using one of the variations.

I am a futures trader living in Chicago. I've worked in the industry for many years, as an exchange employee, order desk clerk, Series 3 broker, and finally as an independent floor trader at the CBOT (MidAm division). I learned much from the veteran traders at the MidAm, but the profit potential of floor trading was limited due to the scarcity of "outside orders" at that exchange. So I took the skills I had picked up from the floor and applied them to off-floor trading. I knew that I had to develop my own system for day trading, as the popular methods around then either didn't work, produced meager profits, or had a low win percentage.

I knew that the old "trend following" and "breakout" methods were unsuitable. Some traders, in interviews or articles, would say things like, "our system only produces a 40% win percentage, but the winning trades more than make up for the losers". To me, that type of trading was absurd.

I, and most normal people, would not want to endure 60% loss percentage. (A coin toss is 50%!).

(Some of the "systems" or "trading courses" still being sold today are based on these outdated principles.)

I became a Series 3 broker at a local FCM. My plan was to advise clients on futures trading while trading my own account. The owners of the firm were unusually tight-fisted about expenses. To cut costs, the brokers had to share quote terminals in groups of 2-3. This particular firm cut costs in other ways, including quality of floor service, which was to cause major problems later on.

But in the meantime, I studied charts and systems, made observations, and traded. I searched for a way to apply the floor trader's "scalping" technique to off-floor trading. The first year was tough, financially, but I made a breakthrough in the second year which led to the first profitable month of day trading I had ever posted. Then, the second month was profitable. And so on. I went from trading the NYFE to the S&P (at that time, the S&P was still $500 per index point). The win-loss ratio of this method was around 9 to 1. One week I made eleven winning trades in a row.

The customer business also picked up, for myself and everyone in the office. The Grain markets of 1996 were taking off and a lot of commissions and new accounts were coming in. We traded the customers all week, and partied every weekend. Some of us flew to Las Vegas, the Caribbean, or Mexico for three-day trips, but tried to be back by at least Tuesday - there was a lot of money to be made.

So I was day trading the S&P and winning, and my account grew, despite the cash withdrawals.

I also collected larger and larger commission checks. I increased my trading size, and even used my methods to day trade Coffee futures, which was a feared market at the time.

That summer I made a return trip to New York City, to visit friends and to live it up in Manhattan, of course. I could afford it now. I returned to Chicago a little hyped, thinking of relocating to Manhattan and trading full-time for a living. I decided to trade my account even more aggressively, increase my profits, and drop the brokerage part of the business, as the customers were becoming time-consuming. Then I would be free to live elsewhere.

I hit the markets hard Monday morning. I got nailed for a quick $450 loss near the open, but I bailed out, and made $600 later that day. I was even more confident, having turned a losing day into a winner. The next two day were all winners. I was ahead $2100 by Wednesday's close.

Thursday was a different story.

I didn't realize it at the time, but the events of that Thursday were foreshadowed by some disasters that had befallen several customers and IB's of the firm.

That spring, the Corn, Wheat, and Soybean markets were the busiest anyone had ever seen (since the 1988 markets, at least) but the floor operation used by our firm was doing a terrible job of handling the flood of orders we sent in. At the CBOT, and the CME as well. As the owners of our firm were obsessed with saving money any way possible, they usually hired the lowest they could find, which was often the worst they could find. Orders that should have been filled were coming back "unable"; orders we thought were unable were being reported as "filled" the following day. Stops were being "blown through" by hundreds of dollars. Customers went "debit"; some threatened lawsuits; one IB trading through us went out of business. I figured I could avoid the madness by staying with the S&P's, which hadn't had major problems up to then.

Well, the problem service reached the S&P, as well. On that Thursday, I placed a limit order to sell. I canceled the order a short time later. I stopped watching the indexes for awhile - the grain customers were keeping me busy. Market action indicated that the S&P order should be "nothing done" - provided it was canceled, on time, by our floor operation. It wasn't.

The sell order was "too late to cancel". That was bad enough. However, due to incompetence and ignorance in both the floor and office operations, the sell was not reported to me for nearly two hours.

To make a long story short, Thursday was a disaster. I was short the S&P without knowing it, and the market was rallying to new highs.

The next mistake was mine. Veteran traders know what I mean; one day you lose perspective, and trade emotionally rather than logically. I was enraged over the operations error, and instead of getting out immediately and salvaging the rest of my account, I attempted to "trade out of it".

I "averaged up" - sold more contracts. The funny thing is, my system called for being long the market - but all logic and reason went out the window that day.

The market continued higher. At the close, my account was "blown out". Eight months of winning trades destroyed by one afternoon of insanity.

I have long since left that firm, and the retail customer business. I am now focused on trading the markets and perfecting my methods.

Things have changed in the futures markets. The size of the S&P contract has been cut in half, and the CME finally introduced a mini S&P, long overdue. Electronic trading and Internet order entry has made precision day trading more feasible - much better than in the old days of phoning in orders.

Real-time quotes are now available over the Internet, along with chart graphics. I'm back on the day trading battlefield. I have refined the method I used back then, and it works even better than before.

FTS 1

FTS 2

FTS 3

FTS 4

FTS 5

FTS 6

FTS 7

FTS 8

FTS 9

FTS 10

FTS 11

FTS 12

FTS 13

FTS 14

FTS 15

FTS 16

borrowed from my good friend NQoos (who borrowed some of my stuff so we're even 🙂)

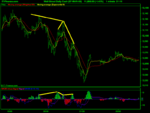

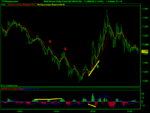

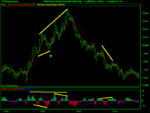

The Floor Trader Futures System - Are you about to pay $3000 for a $500 trading system?

Futures trading courses and systems are offered for sale at prices ranging from a few hundred dollars to several thousand dollars.

Many of these trading methods are not new or original. Often they are based on information found in trading books or articles written decades ago. In some cases they are old trading methods repackaged in new books (or made into software), and sold at high prices.

The original sources of these methods are sometimes obscure and unknown to the general public.

If you know where to look, however, some of these high-priced futures trading systems can be traced back to their original source - at a much lower price.

And there are some trading methods, of recent design, known only to a few Chicago traders, the few that actually make a living from trading - rather than from hawking books, software, and seminars.

I am an ex-floor trader and broker living in Chicago.

The basis of this system was told to me several years ago by a veteran floor trader at the Mid- America exchange in Chicago. He had two futures accounts: one for his day trading, and another for "position" trading, using this method almost exclusively. He was a millionaire and traded large positions, but he started his career with a small account. He made the millions from the market, using his methods, over several years. (He was a contemporary of Richard Dennis). He didn't mention who created the system.

The system was originally created for position trading. I developed some variations which work for day trading stock index futures.

Variations of this trading system are known to a handful of people in the Chicago trading community. I have been told of one individual who charges $1000 for instruction, using one of the variations.

The Floor Trader Method

A STORY FROM THE TRADING BATTLEFIELD

A STORY FROM THE TRADING BATTLEFIELD

I am a futures trader living in Chicago. I've worked in the industry for many years, as an exchange employee, order desk clerk, Series 3 broker, and finally as an independent floor trader at the CBOT (MidAm division). I learned much from the veteran traders at the MidAm, but the profit potential of floor trading was limited due to the scarcity of "outside orders" at that exchange. So I took the skills I had picked up from the floor and applied them to off-floor trading. I knew that I had to develop my own system for day trading, as the popular methods around then either didn't work, produced meager profits, or had a low win percentage.

I knew that the old "trend following" and "breakout" methods were unsuitable. Some traders, in interviews or articles, would say things like, "our system only produces a 40% win percentage, but the winning trades more than make up for the losers". To me, that type of trading was absurd.

I, and most normal people, would not want to endure 60% loss percentage. (A coin toss is 50%!).

(Some of the "systems" or "trading courses" still being sold today are based on these outdated principles.)

I became a Series 3 broker at a local FCM. My plan was to advise clients on futures trading while trading my own account. The owners of the firm were unusually tight-fisted about expenses. To cut costs, the brokers had to share quote terminals in groups of 2-3. This particular firm cut costs in other ways, including quality of floor service, which was to cause major problems later on.

But in the meantime, I studied charts and systems, made observations, and traded. I searched for a way to apply the floor trader's "scalping" technique to off-floor trading. The first year was tough, financially, but I made a breakthrough in the second year which led to the first profitable month of day trading I had ever posted. Then, the second month was profitable. And so on. I went from trading the NYFE to the S&P (at that time, the S&P was still $500 per index point). The win-loss ratio of this method was around 9 to 1. One week I made eleven winning trades in a row.

The customer business also picked up, for myself and everyone in the office. The Grain markets of 1996 were taking off and a lot of commissions and new accounts were coming in. We traded the customers all week, and partied every weekend. Some of us flew to Las Vegas, the Caribbean, or Mexico for three-day trips, but tried to be back by at least Tuesday - there was a lot of money to be made.

So I was day trading the S&P and winning, and my account grew, despite the cash withdrawals.

I also collected larger and larger commission checks. I increased my trading size, and even used my methods to day trade Coffee futures, which was a feared market at the time.

That summer I made a return trip to New York City, to visit friends and to live it up in Manhattan, of course. I could afford it now. I returned to Chicago a little hyped, thinking of relocating to Manhattan and trading full-time for a living. I decided to trade my account even more aggressively, increase my profits, and drop the brokerage part of the business, as the customers were becoming time-consuming. Then I would be free to live elsewhere.

I hit the markets hard Monday morning. I got nailed for a quick $450 loss near the open, but I bailed out, and made $600 later that day. I was even more confident, having turned a losing day into a winner. The next two day were all winners. I was ahead $2100 by Wednesday's close.

Thursday was a different story.

I didn't realize it at the time, but the events of that Thursday were foreshadowed by some disasters that had befallen several customers and IB's of the firm.

That spring, the Corn, Wheat, and Soybean markets were the busiest anyone had ever seen (since the 1988 markets, at least) but the floor operation used by our firm was doing a terrible job of handling the flood of orders we sent in. At the CBOT, and the CME as well. As the owners of our firm were obsessed with saving money any way possible, they usually hired the lowest they could find, which was often the worst they could find. Orders that should have been filled were coming back "unable"; orders we thought were unable were being reported as "filled" the following day. Stops were being "blown through" by hundreds of dollars. Customers went "debit"; some threatened lawsuits; one IB trading through us went out of business. I figured I could avoid the madness by staying with the S&P's, which hadn't had major problems up to then.

Well, the problem service reached the S&P, as well. On that Thursday, I placed a limit order to sell. I canceled the order a short time later. I stopped watching the indexes for awhile - the grain customers were keeping me busy. Market action indicated that the S&P order should be "nothing done" - provided it was canceled, on time, by our floor operation. It wasn't.

The sell order was "too late to cancel". That was bad enough. However, due to incompetence and ignorance in both the floor and office operations, the sell was not reported to me for nearly two hours.

To make a long story short, Thursday was a disaster. I was short the S&P without knowing it, and the market was rallying to new highs.

The next mistake was mine. Veteran traders know what I mean; one day you lose perspective, and trade emotionally rather than logically. I was enraged over the operations error, and instead of getting out immediately and salvaging the rest of my account, I attempted to "trade out of it".

I "averaged up" - sold more contracts. The funny thing is, my system called for being long the market - but all logic and reason went out the window that day.

The market continued higher. At the close, my account was "blown out". Eight months of winning trades destroyed by one afternoon of insanity.

I have long since left that firm, and the retail customer business. I am now focused on trading the markets and perfecting my methods.

Things have changed in the futures markets. The size of the S&P contract has been cut in half, and the CME finally introduced a mini S&P, long overdue. Electronic trading and Internet order entry has made precision day trading more feasible - much better than in the old days of phoning in orders.

Real-time quotes are now available over the Internet, along with chart graphics. I'm back on the day trading battlefield. I have refined the method I used back then, and it works even better than before.

FTS 1

FTS 2

FTS 3

FTS 4

FTS 5

FTS 6

FTS 7

FTS 8

FTS 9

FTS 10

FTS 11

FTS 12

FTS 13

FTS 14

FTS 15

FTS 16

borrowed from my good friend NQoos (who borrowed some of my stuff so we're even 🙂)