- Cohn resignation puts 'trade wars' front and central once again; digesting

Oz GDP, central bank comments, awaiting China FX reserves, US ADP Employment,

Beige Book, Malaysia, Turkey, Poland and Canada rate decisions' Germany to

sell 5-yr, busier day for corporate earnings

- 'Trade war' fears locks horns with excess liquidity from QE and share

buybacks to give volatility some levitation

- US Beige Book / Brainard: Brainard shift to a hawkish lean likely to

overshadow likely upbeat Beige Book

- US ADP Employment: seen posting 200K plus gain for sixth month in seven,

quite a feat at this mature stage of the economic cycle

- Canada rates: BoC set to underline that it is data and NAFTA dependent,

may sound less optimistic on outlook

- Poland rates: no change expected, inflation forecast likely to reaffirm

neutral policy outlook for 2019

..........................................................................

********************

** EVENTS PREVIEW **

********************

Today's schedule is rather busier, above all in central bank terms, though there are a number of data items, which may catch the attention of markets, and offer some distraction from politics. Statistically, there is the Australian Q4 GDP to digest ahead of China FX Reserves, the detailed breakdown on Eurozone Q4 GDP, US ADP Employment, US and Canadian Trade, while tonight brings the revised Japan Q4 GDP. There are rate decisions in Malyasia, Turkey, Poland and Canada, with the Fed publishing its Beige Book and Bostic the only Fed speaker, while Germany sells 5-yr OBL. A busier day corporate earnings has Deutsche Post, Rolls Royce & Telecom Italia in Europe, while across the pond Brown-Forman, Costco and Dollar Tree should attract some attention. However with NEC chair Cohn resigning due to his opposition to the steel and aluminium tariffs, it is likely that 'trade wars' will be the dominant theme for the day. But he point remains that while markets may be fearful of 'trade wars', there is still far too much of that central bank excess liquidity (#QE) floating around markets, which now combines with the up to $800 Bln of share buyback monies due to the tax reform, which os desperately looking for a home, pretty much regardless of risks, and as such many will construct a more positive story as an excuse to put that money work, buying dips and adding to risk positions... eminently this is building a large silo of troubles ahead. But in the first instance this is a recipe for a sustained uplift for volatility.

** Poland - NBP rate decision and forecast update **

- As previously noted, the NBP retains a very dovish bias, placing far greater weight on subdued inflation, and seeing little reason to respond to strong growth, a tight labour market and robust real wage growth. As such it is no surprise that the NBP is not expected to move rates from the current 1.50%, or that markets are only discounting an initial rate move in Q1 2019. Today's meeting will also see a fresh set of NBP forecasts, which are unlikely to see any sharp revisions, though they will be combed for anything that might open the possibility of an initial rate move being brought forward.

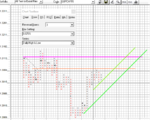

** Canada - BoC rate decision **

- Markets have been pushing sharply back on the BoC's rate trajectory, on a combination of weaker than expected growth data, well behaved inflation and rising concerns about NAFTA negotiations, most recently punctuated by Trump's trade tariffs Which would hit Canada hardest. Having discounted a 64% probability of an April 18 meeting 25 bps rate hike in mid-February (see chart), this is now seen as a 34% probability - little wonder that the CAD is at an 8-month low vs the USD. Poloz and co. have turned rather more cautious after a run of three rate hikes to 1.25%, and underlining that the rate trajectory will be relatively fluid and highly data dependent, and as Poloz noted in February very NAFTA dependent "We've got a drag on investment that's already in place because of the uncertainty around NAFTA". This is not a forecast update meeting, and as such the focus will be on extent to which the statement highlights the risk of forecasts needing to be revised lower, or not, as the case may be.

** U.S.A. - February ADP Employment / Beige Book **

- It has not escaped the attention of many market participants, that the once mighty data juggernaut that is the US labour market report has elicited far more 'meh' reactions over the past year, than being the prompt for any sharp or volatile market moves. Be that as it may, there are many who view this Friday's report as potentially critical, though primarily in terms of the wages component (seen at 0.3% m/m for an unchanged 2.9% y/y), particularly given the much discussed distortions to January's higher than expected reading, due to bad weather effects. Be that as it may, today's ADP Private Employment estimate is projected to see a 200K increase, which would be the 6h month in the past seven, with an increase of 20OK plus (September being the exception at +6K) - really quite remarkable at this stage of the economic cycle, and with the Unemployment Rate at a multi-decade low of 4.1%. The Beige Book remains the most comprehensive overview of the US economy, and will doubtless paint a picture of solid 'modest or moderate growth', with the focus on signals on wages, labour demand and prices along with the level business optimism on the outlook. Of specific interest will be the reports on agriculture in those regions most heavily impacted by the drought in the grains regions. However, it is the relatively sharp shift from very dovish to modestly hawkish from Fed governor Brainard, as detailed in her speech last night, which is likely to be the main discussion point, in so far as it underlines that the bar to the Fed reverting to the dovish tone that has been dominant over the past decade now looks to be very high. Notably Brainard referenced loose financial conditions in addition to what she termed a shift from "headwinds" to "tailwinds" for the economy as a whole.

** Japan - Q4 revised GDP **

- In the wake of yet another better expected set of Q4 CapEx reading (headline 4.3% y/y, ex-Software 4.7% y/y), Q4 GDP is expected to be revised up from 0.5% SAAR to 1.0% (or 0.2% q/q), with the risks as was the case with the Q3 GDP revision modestly to the upside of estimates. This will however not deter the BoJ from sticking to the line that there will be no discussion on exit timing (though plenty on exit strategy), until the CPI target of 2.0% is clearly being met.

from Marc Ostwald