pedro01

Guest

- Messages

- 1,058

- Likes

- 150

I am looking to take control of my pension, cash part of it in and manage it myself. The management will be more passive than anything else.

This has nothing to do with my trading. For my long-term money, I do not want to be actively trading it, even with swing trades. I don't quite trust myself. I have had other people managing my money and have decided that I don't trust them either !

The time horizon I am looking at is 20 years.

Asset allocation will be part of my strategy and I will get into that later but also I am looking at forms of money management to help in my quest.

As this will be mostly a passive approach. ETFs will be used and they will be passive tracker-type ETFs for each asset class I choose (e.g. property, fixed income, equity, commodity etc).

There is a fundamental issue with this approach and it can be summed up as follows:

Basically the S&P is now at the same level it is at 10 years ago. That's 10 years with zero return, in fact less than zero when you consider inflation.

So - how do you overcome this ? If you allocate across 5 asset classes and one of them does this, that means 20% of your portfolio could go nowhere for 10 years.

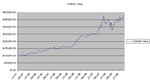

Now look at the following, with a little bit of "Money Management Mystique" thrown in, the following results are possible for the same time period:

That leaves us with a current balance of $136,376.58 on an investment of $100,000 and also leaves us with 1,111 shares. Note that if you'd put $100,000 into the SPY on the start date above, you'd be sitting on roughly $100,000 and 1,000 shares. That's 36% more money & 10% more shares on hand.

So - how exactly was this done ? Basically, it is using a money management technique known as AIM.

Let's say you have $100,000 to invest. AIM dictates that you actually only put a percentage of that into the investment (in this example, 50%) and then put 50% into an interest bearing account. Then once a month/quarter, you review the value and buy/sell stocks as AIM rules dictate. You are not trying to time the market, you are just doing some math once a month and either moving stocks to cash or vice-versa.

The actual rules are here : Core Position Trading™ (CPT), Robert Lichello's Automatic Investment Management (AIM) Basics (Stocks, ETFs, and Mutual Funds)

Spreadsheet for the above is also attached. Note that I am using an adjusted version of AIM which does not allow you to buy more than your cash reserve. AIM isn't perfect.

There are some variations on AIM and I have ordered a few books on similar topics but there isn't much out there. I am currently unsure as to which model is best but I think the following points are relevant:

1 - All models will probably reduce returns of an instrument that goes straight up for 20 years.

2 - No model will provide a positive return of an instrument that goes straight down for 20 years

3 - No model, will provide a positive return of an instrument that flatlines for 20 years (of course 'buy & write' would do this but it isn't passive)

4 - Dollar cost averaging will not be considered

Anyway - at this point, if any of you have any models you think are worth considering, let me know. Otherwise, I'll start researching.

This has nothing to do with my trading. For my long-term money, I do not want to be actively trading it, even with swing trades. I don't quite trust myself. I have had other people managing my money and have decided that I don't trust them either !

The time horizon I am looking at is 20 years.

Asset allocation will be part of my strategy and I will get into that later but also I am looking at forms of money management to help in my quest.

As this will be mostly a passive approach. ETFs will be used and they will be passive tracker-type ETFs for each asset class I choose (e.g. property, fixed income, equity, commodity etc).

There is a fundamental issue with this approach and it can be summed up as follows:

Basically the S&P is now at the same level it is at 10 years ago. That's 10 years with zero return, in fact less than zero when you consider inflation.

So - how do you overcome this ? If you allocate across 5 asset classes and one of them does this, that means 20% of your portfolio could go nowhere for 10 years.

Now look at the following, with a little bit of "Money Management Mystique" thrown in, the following results are possible for the same time period:

That leaves us with a current balance of $136,376.58 on an investment of $100,000 and also leaves us with 1,111 shares. Note that if you'd put $100,000 into the SPY on the start date above, you'd be sitting on roughly $100,000 and 1,000 shares. That's 36% more money & 10% more shares on hand.

So - how exactly was this done ? Basically, it is using a money management technique known as AIM.

Let's say you have $100,000 to invest. AIM dictates that you actually only put a percentage of that into the investment (in this example, 50%) and then put 50% into an interest bearing account. Then once a month/quarter, you review the value and buy/sell stocks as AIM rules dictate. You are not trying to time the market, you are just doing some math once a month and either moving stocks to cash or vice-versa.

The actual rules are here : Core Position Trading™ (CPT), Robert Lichello's Automatic Investment Management (AIM) Basics (Stocks, ETFs, and Mutual Funds)

Spreadsheet for the above is also attached. Note that I am using an adjusted version of AIM which does not allow you to buy more than your cash reserve. AIM isn't perfect.

There are some variations on AIM and I have ordered a few books on similar topics but there isn't much out there. I am currently unsure as to which model is best but I think the following points are relevant:

1 - All models will probably reduce returns of an instrument that goes straight up for 20 years.

2 - No model will provide a positive return of an instrument that goes straight down for 20 years

3 - No model, will provide a positive return of an instrument that flatlines for 20 years (of course 'buy & write' would do this but it isn't passive)

4 - Dollar cost averaging will not be considered

Anyway - at this point, if any of you have any models you think are worth considering, let me know. Otherwise, I'll start researching.

Attachments

Last edited: