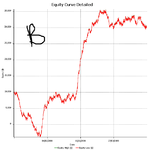

And B - Equity Curve and details.

Note B loses more than enough money to begin with, which leads me to believe that the Gap grades were a large component of the PnL.

Both examples are with same commissions and slippage, no compounding.

Now clearly what works for A doesn't work for B, but:

*Included in the backtest are somewhat arbitrary variables (that is, I chose them from experience having traded these "manually" and haven't changed them). If I change these variables for B, how do I avoid curve fitting them?

*A and B are different asset classes, there is no reason to expect what works on one will work on another

*changing the slippage to something more likely improves the performance dramatically

Thoughts?

Note B loses more than enough money to begin with, which leads me to believe that the Gap grades were a large component of the PnL.

Both examples are with same commissions and slippage, no compounding.

Now clearly what works for A doesn't work for B, but:

*Included in the backtest are somewhat arbitrary variables (that is, I chose them from experience having traded these "manually" and haven't changed them). If I change these variables for B, how do I avoid curve fitting them?

*A and B are different asset classes, there is no reason to expect what works on one will work on another

*changing the slippage to something more likely improves the performance dramatically

Thoughts?