You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Best Thread Arabian's *serious* Thread

- Thread starter arabianights

- Start date

- Watchers 25

arabianights

Legendary member

- Messages

- 6,721

- Likes

- 1,380

DashRiprock

Experienced member

- Messages

- 1,650

- Likes

- 482

Re: 101 ways to kill a cat

arabian about short sterling notional... has it always been 500 large? did any of the specifications change when it went back to full ticks?

and

are you the best trader on trade to win?

🙂

arabian about short sterling notional... has it always been 500 large? did any of the specifications change when it went back to full ticks?

and

are you the best trader on trade to win?

🙂

arabianights

Legendary member

- Messages

- 6,721

- Likes

- 1,380

Re: 101 ways to kill a cat

will only answer questions on my thread

(not being a dick, just don't want to contaminate this one more, and answering this would "set a precedent" if you get me)

arabian about short sterling notional... has it always been 500 large? did any of the specifications change when it went back to full ticks?

and

are you the best trader on trade to win?

🙂

will only answer questions on my thread

(not being a dick, just don't want to contaminate this one more, and answering this would "set a precedent" if you get me)

DashRiprock

Experienced member

- Messages

- 1,650

- Likes

- 482

Re: 101 ways to kill a cat

i didnt want to ask on your thread cos its off topic and i have marked your thread as a "no lulz zone" so i will be careful about what i write

i didnt want to ask on your thread cos its off topic and i have marked your thread as a "no lulz zone" so i will be careful about what i write

arabianights

Legendary member

- Messages

- 6,721

- Likes

- 1,380

Re: 101 ways to kill a cat

Always so long as I've been trading it... and to be honest the half tick time was fantastic fun... not sure how much of that was due to general credit crunch lack of liquidity and how much was cause annoying huge size spreaders had to **** off but trading outrights you could scalp with .5 stops and 1.5 targets... fantastic!

categorically not, alas 🙁

arabian about short sterling notional... has it always been 500 large? did any of the specifications change when it went back to full ticks?

Always so long as I've been trading it... and to be honest the half tick time was fantastic fun... not sure how much of that was due to general credit crunch lack of liquidity and how much was cause annoying huge size spreaders had to **** off but trading outrights you could scalp with .5 stops and 1.5 targets... fantastic!

are you the best trader on trade to win?

categorically not, alas 🙁

arabianights

Legendary member

- Messages

- 6,721

- Likes

- 1,380

Re: 101 ways to kill a cat

Lulz are SUPER welcome on my thread. If it gets absolutely ridiculous I will hypocritically complain about it, but in general more lulz the better!

i didnt want to ask on your thread cos its off topic and i have marked your thread as a "no lulz zone" so i will be careful about what i write

Lulz are SUPER welcome on my thread. If it gets absolutely ridiculous I will hypocritically complain about it, but in general more lulz the better!

DashRiprock

Experienced member

- Messages

- 1,650

- Likes

- 482

(continued...)

Arabian, are you the best trader on trade to win?

🙂

as well good luck trading from home, its can be very easy for trading life and other life to all blur into a homogeneous gloop of antilulz.

Arabian, are you the best trader on trade to win?

🙂

as well good luck trading from home, its can be very easy for trading life and other life to all blur into a homogeneous gloop of antilulz.

arabianights

Legendary member

- Messages

- 6,721

- Likes

- 1,380

(continued...)

Arabian, are you the best trader on trade to win?

🙂

as well good luck trading from home, its can be very easy for trading life and other life to all blur into a homogeneous gloop of antilulz.

Absolutely everyone is telling me this. I can't say this to people in my office cause it'll sound very rude, I have to pretend I share their concerns, but I can say it on the internet: Although you'd think the complete opposite if you knew me, I'm a natural introvert in the sense I don't care about talking to people... Total silence during the day will be fine by me 🙂

In any case I should have a better social life trading from home given that I'll have more time in the evenings... it's ridiculous the amount of occasions I can't make due to these early starts that I will be able to once this is sorted.

Martinghoul

Senior member

- Messages

- 2,691

- Likes

- 277

I think you should tell everyone about your adventures in front Swizzer. Way more fun than sh1t stg.

Thanks for a very interesting trade narrative. I don't trade rates so please bear with me.

From the tick chart it looks like the seller of 11,000 contracts @ 14 did this more or less instantly. Nevertheless they didn't go through the bids; ie they got a 'very large trade' done quickly at 14. That suggests a lot of liquidity at that level. Do you normally see that much liquidity?

After the big order how soon did you enter your trade?

From the tick chart it looks like the seller of 11,000 contracts @ 14 did this more or less instantly. Nevertheless they didn't go through the bids; ie they got a 'very large trade' done quickly at 14. That suggests a lot of liquidity at that level. Do you normally see that much liquidity?

After the big order how soon did you enter your trade?

wackypete2

Legendary member

- Messages

- 10,211

- Likes

- 2,058

I didn't know Arabian was a trader too!

Anyway, good stuff 👍

Peter

Anyway, good stuff 👍

Peter

scose-no-doubt

Veteren member

- Messages

- 4,630

- Likes

- 954

I think you should tell everyone about your adventures in front Swizzer. Way more fun than sh1t stg.

Lets keep it civil, son. Less of the slang. Or else.

kimo'sabby

Experienced member

- Messages

- 1,622

- Likes

- 287

Arabian,

Could you give us a brief history of how you came about trading your particular market. Does your firm specialise in stirs, how you came about having an interest in the markets, etc.

Tbh, i think you need to do an interview with t2w (if you havent already). Give this whole thing some logical structure.

A consideration maybe.

Could you give us a brief history of how you came about trading your particular market. Does your firm specialise in stirs, how you came about having an interest in the markets, etc.

Tbh, i think you need to do an interview with t2w (if you havent already). Give this whole thing some logical structure.

A consideration maybe.

Trader333

Moderator

- Messages

- 8,766

- Likes

- 1,030

Tbh, i think you need to do an interview with t2w (if you havent already)

This has already been done but AN did not wish to have it published.

Paul

scose-no-doubt

Veteren member

- Messages

- 4,630

- Likes

- 954

Who cares what his wishes are? Post it.

He constantly clogs the boards with filth and so it's about time he did something like this 😀

He constantly clogs the boards with filth and so it's about time he did something like this 😀

kimo'sabby

Experienced member

- Messages

- 1,622

- Likes

- 287

This has already been done but AN did not wish to have it published.

Paul

I think he maybe worried about losing his t2w personna.

arabianights

Legendary member

- Messages

- 6,721

- Likes

- 1,380

I think you should tell everyone about your adventures in front Swizzer. Way more fun than sh1t stg.

I don't 😆

Thanks for a very interesting trade narrative. I don't trade rates so please bear with me.

From the tick chart it looks like the seller of 11,000 contracts @ 14 did this more or less instantly. Nevertheless they didn't go through the bids; ie they got a 'very large trade' done quickly at 14. That suggests a lot of liquidity at that level. Do you normally see that much liquidity?

After the big order how soon did you enter your trade?

I wasn't actually watching the order book so can't say for certain but I would imagine that it was already a bit low for other contracts so much of the bid was implied. Size on a bid or offer is partly subject to a positive feedback loop due to the reasons I already mentioned about traders and algos angling for fills. In those circumstances (particularly the it being out of line with other contracts) that liquidity is not unusual but it would be unusual otherwise that far down the strip. At the moment it is 3399x 1585 including implieds, or about 2000 x 1000 in the outright. Certainly it essentially went through the bid - there wasn't "really" that much there.

And I would have entered the trade after a few minutes - I wanted to see the algos doing what I expected them to.

Arabian,

Could you give us a brief history of how you came about trading your particular market. Does your firm specialise in stirs, how you came about having an interest in the markets, etc.

Tbh, i think you need to do an interview with t2w (if you havent already). Give this whole thing some logical structure.

A consideration maybe.

Yup, the part of my firm I joined specialises in them so I didn't have much choice. As for interest in markets... er, I wanted to make money and saw an add in university careers service website... 😆

I've since developed an interest in the markets from having the job (and a general interest in politics and current events, which I would argue is the same thing) but I wouldn't say I had it before.

DashRiprock

Experienced member

- Messages

- 1,650

- Likes

- 482

I don't 😆

I wasn't actually watching the order book so can't say for certain but I would imagine that it was already a bit low for other contracts so much of the bid was implied. Size on a bid or offer is partly subject to a positive feedback loop due to the reasons I already mentioned about traders and algos angling for fills. In those circumstances (particularly the it being out of line with other contracts) that liquidity is not unusual but it would be unusual otherwise that far down the strip. At the moment it is 3399x 1585 including implieds, or about 2000 x 1000 in the outright. Certainly it essentially went through the bid - there wasn't "really" that much there.

And I would have entered the trade after a few minutes - I wanted to see the algos doing what I expected them to.

Yup, the part of my firm I joined specialises in them so I didn't have much choice. As for interest in markets... er, I wanted to make money and saw an add in university careers service website... 😆

I've since developed an interest in the markets from having the job (and a general interest in politics and current events, which I would argue is the same thing) but I wouldn't say I had it before.

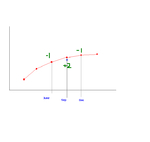

if nobody minds i will try and explain what this means a bit more because if you didnt know about stirs and implieds it might not make any sense. Its also good for me to check that i am understanding you right 👍

So, what arabian means by "it was already a bit low for other contracts"... STIRS are interest rate futures on 3 month LIBOR. One thing about this market is that, for example, you wanted to find out how much it would cost to borrow 500k (the notional of the contract) for 1 year starting from January 2012, you just use the four 3 month rates in a row (so you would do Jan -> March, March -> June, June -> Sept and Sept -> Dec).

when you plot the prices for all of the contracts on a graph, that is what is called the yield curve, and represents the different cost of borrowing for different lengths of time. If you watch the pic I did, what he means is that the SEPT '12 future was a bit low compared to the other contracts either side of it (the blue dot).

Right, another thing - when he says "the bid was implied". In STIRS you cn not just trade the futures on their own, but you can as well trade more than one future in the same trade. So, the simplest example is a calendar spread, which is like LONG March SHORT June. there types of trade are for trading non-parrales shifts in the yield curve (like one goes up or down more than the other).

What is special about these is that the you can make an order for the whole spread, you dont have to make orders for both futures (this is called legging in and legging out) If, say, the March - June spread was at 7, i could place a order on exchange to buy it at 5, and the exchange would automatically jiggle two orders in the individual futures so that i was always ordering a difference of 5. when this happens, the orders show up on the individual futures as well as for the orderbook on the spread. The orders I have put on the individual futures are called "implied", because they are implied from what i am ordering the spread for.

So, in this case because the future is out of line with the other ones, there will probably be lots of traders either trying to trade the calendar spread (or a butterfly, two spread in a row) so try and make profits from when it goes back into line. there orders for spreads would show up in the individual SEP orderbook, but these are implied from the orders actually wanting to trade the spreads. Like here there could be lots of orders wanting to do "Sell 1 x June, but 2 x Sep, sell 1 x Dec" for a butterfly that will bake profits if the blue dot gets back into line with the red ones - these are the implieds on the bid.

there is also implied in and implied out and even implieds on implieds but thats a but tricky. hope that I understood it right arabian and it helps anyone who doesnt know stirs.

Attachments

Similar threads

- Replies

- 2

- Views

- 8K

- Replies

- 27

- Views

- 7K

- Replies

- 775

- Views

- 221K