L

Liquid validity

The best variant so far (I use the term loosely...😆 ).

H1

UK 07:00-10:00

USA 13:00-15:30

30 point stop loss.

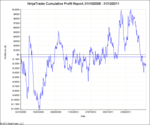

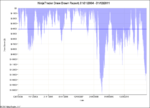

Again though, largely worthless - look at the Drawdown chart - hideous

For that reason, just in case anyone is thinking of using this:

Drawdown is excessive for a 1 lot.

Also, its just a backtest, no monte carlo, bootstrapping or forward testing has been done.

The source code text file gives you an idea of the end result.

So maybe Heiken Ashi has some merit, or is it more to do with cutting losses

and controlling entry time...🙂

H1

UK 07:00-10:00

USA 13:00-15:30

30 point stop loss.

Again though, largely worthless - look at the Drawdown chart - hideous

For that reason, just in case anyone is thinking of using this:

Drawdown is excessive for a 1 lot.

Also, its just a backtest, no monte carlo, bootstrapping or forward testing has been done.

The source code text file gives you an idea of the end result.

So maybe Heiken Ashi has some merit, or is it more to do with cutting losses

and controlling entry time...🙂

Attachments

Last edited: