-oo0(GoldTrader)

Well-known member

- Messages

- 345

- Likes

- 5

Spread within a spread.

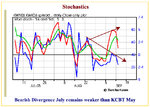

When you are rolling up or adding a spread it may help to look at the “spread within a spread.” Traders that exchange email with me are familiar with the concept. Suppose you are in a seasonal spread. The time comes to add another spread with one side remaining the same. What you do is plot the “spread within the spread,” and use normal chart analysis to roll up or just initiate new positions in the side you are changing.

For example the “inner spread,” in seasonal KCBT wheat still favors shorting July instead of the less liquid May or March against December.

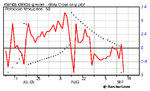

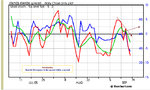

When you are rolling up or adding a spread it may help to look at the “spread within a spread.” Traders that exchange email with me are familiar with the concept. Suppose you are in a seasonal spread. The time comes to add another spread with one side remaining the same. What you do is plot the “spread within the spread,” and use normal chart analysis to roll up or just initiate new positions in the side you are changing.

For example the “inner spread,” in seasonal KCBT wheat still favors shorting July instead of the less liquid May or March against December.