You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

lifestatic

Newbie

- Messages

- 8

- Likes

- 0

Dear JonnyT,

Could you detail this strat?

I guess I missed something earlier.

Breakout of 7:00-10:00 AM UK time?

What T/P?

Any trailing stops?

Break/E at when if any?

Could you detail this strat?

I guess I missed something earlier.

Breakout of 7:00-10:00 AM UK time?

What T/P?

Any trailing stops?

Break/E at when if any?

JonnyT said:Again a breakout of the 07:00 to 10:00 bar. This time EUR/USD March contract, varying stop losses:

Stop Profit Loss

10 536 82

15 670 120

20 916 140

25 891 175

30 1031 180

35 1126 164

40 1021 189

45 989 182

50 960 202

60 1075 242

JonnyT

Hi JT,

I take it the "loss " column is the max drawdown ?

the numbers look pretty good , are these actual results or backtests ?

cheers

Ian

JonnyT said:eer, the first post is nearly a year old!!!!

I think T2W Admin have just been playing about.

Doohhhh

TWI

Senior member

- Messages

- 2,562

- Likes

- 269

FetteredChinos

Veteren member

- Messages

- 3,897

- Likes

- 40

i'd be looking to short below 20,000

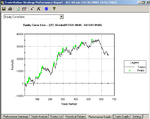

surprised the equity curve has tailed off so much though. at worst i thought it would be at least flat..

FC

surprised the equity curve has tailed off so much though. at worst i thought it would be at least flat..

FC

TWI

Senior member

- Messages

- 2,562

- Likes

- 269

It is because when there is no trend short term spikes do not follow through. As a result break-out systems will get in on a short term spike and then get caught. I think some small adjustment of the system entry rules could solve this but at the same time it will also substantially decrease the trending performance. Over time this system may well end up in net profit but whether anybody can follow it through this sort of pain is another question. I think the key is diversification of system and of product. Never put all eggs in one basket no matter how good it might look in the short term.

FetteredChinos

Veteren member

- Messages

- 3,897

- Likes

- 40

i know why breakout systems dont work tw, but the ones i have tested in the past, when they go awry, the worst they seem to do is just level off.

what do you suggest to filter the entries?? establish a long/short bias? and trade say a 7-9 breakout to the biased side, or the 7-10 breakout to the short side?

havent looked at that in the past, and it only just hit me. might be worth a look.

fc

what do you suggest to filter the entries?? establish a long/short bias? and trade say a 7-9 breakout to the biased side, or the 7-10 breakout to the short side?

havent looked at that in the past, and it only just hit me. might be worth a look.

fc

TWI

Senior member

- Messages

- 2,562

- Likes

- 269

Yeah, sorry FC, I know you are well aware of all this stuff, It is just that this characteristic is very evident with this system when looking back over this year-to-date.

I tend to consider everything a range trade but look to daily and weekly levels rather than 60min ones to determine a break. I still use intraday data to generate signals. I have not solved the problem in any clever way but I do trade a portfolio of 4 currencies using a fairly simple system, less than 2 pages of code. This is EUR/GBP/CHF/JPY despite the fact that they are all traded against the USD the correlation between the markets is no more than 0.4 in worst case, this between EUR & CHF, for others it is far lower. I would find it hard to trade any individual pair but the combined result limits drawdowns to ~8.5% at worst. despite having >18% draw in one component (GBP). I certainly underpeformed the breakout system last year but I am also up 9% YTD. and not feeling so inferior anymore. I only started trading this last year however so there is of course every chance it could all go horribly wrong.

I tend to consider everything a range trade but look to daily and weekly levels rather than 60min ones to determine a break. I still use intraday data to generate signals. I have not solved the problem in any clever way but I do trade a portfolio of 4 currencies using a fairly simple system, less than 2 pages of code. This is EUR/GBP/CHF/JPY despite the fact that they are all traded against the USD the correlation between the markets is no more than 0.4 in worst case, this between EUR & CHF, for others it is far lower. I would find it hard to trade any individual pair but the combined result limits drawdowns to ~8.5% at worst. despite having >18% draw in one component (GBP). I certainly underpeformed the breakout system last year but I am also up 9% YTD. and not feeling so inferior anymore. I only started trading this last year however so there is of course every chance it could all go horribly wrong.

twalker said:ianp - Hi, are you in Oz yet?

Since we are digging up the past, here is an updated equity curve. Just demonstrates how breakout systems under-perform in sideways markets. A lot of hedge funds have been caught in this one too.

Hi TW,

Yes I am in Oz , I am living on the Sunshine Coast in Qld,

It a pretty nice place to be .

Thanks for the chart , best leave that one alone !!!!!!!!

Cheers

Ian

TWI

Senior member

- Messages

- 2,562

- Likes

- 269

Sounds fantastic. One day I hope to have it in me to make a move like that.

Apart from the sky being upside down it must mean you can make the most of the sunshine due to the timezone.

To save you time, if you are also investigating SIBKIS leave that alone for now too. Currently made nothing since August 04.

Ask yourself why does the code I have attached work on BP and EC during the same period?

Note this is TS8 code so will need to adjust for TS2000.

----------------------------------------------------------------------------------------------------------------------------

RISK DISCLOSURE

Not for solicitation purposes. The risk of trading futures contracts can be substantial. You should therefore, carefully consider whether such trading is suitable for you in light of your circumstances and financial resources. The information contained herein contains statements that are the opinion of the author. Past performance is not necessarily indicative of future results.

Apart from the sky being upside down it must mean you can make the most of the sunshine due to the timezone.

To save you time, if you are also investigating SIBKIS leave that alone for now too. Currently made nothing since August 04.

Ask yourself why does the code I have attached work on BP and EC during the same period?

Note this is TS8 code so will need to adjust for TS2000.

----------------------------------------------------------------------------------------------------------------------------

RISK DISCLOSURE

Not for solicitation purposes. The risk of trading futures contracts can be substantial. You should therefore, carefully consider whether such trading is suitable for you in light of your circumstances and financial resources. The information contained herein contains statements that are the opinion of the author. Past performance is not necessarily indicative of future results.

Attachments

alpha_monkey

Member

- Messages

- 97

- Likes

- 5

JonnyT said:Ve hav vays of making it verk...

JonnyT

Have noted your posts with interest for a while.

Any recent insights you can share on making it verk?

AM